CONSENT TO USE OF COOKIES ON INITIAL ACCESS TO THE WEB SITE

Snam uses cookies as part of this site to ensure an excellent browsing experience. This site also uses third-party cookies. The cookies used cannot identify the user. For more information about the cookies used and how to delete them, click here. By continuing to browse this site, you consent to the use of cookies.

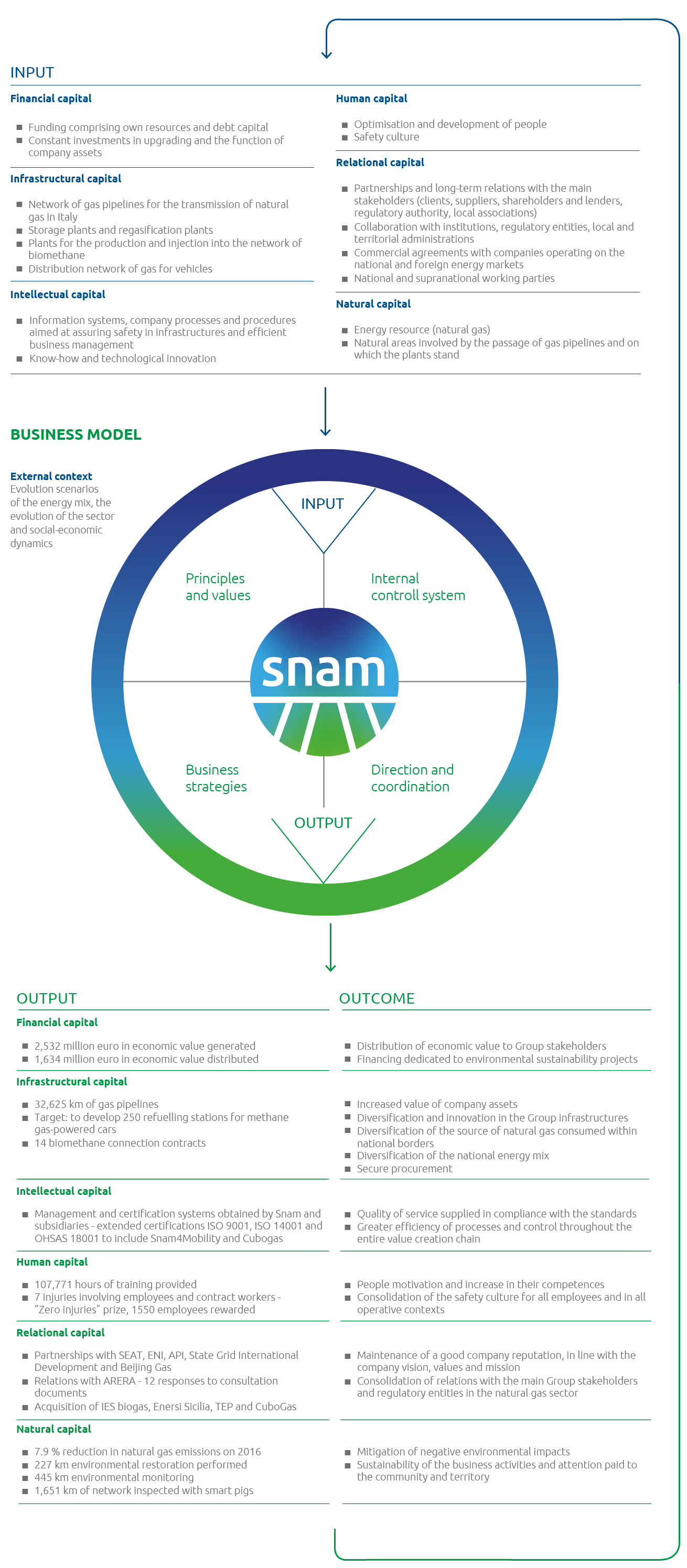

Creating sustainable value: the Snam business model

Financial capital

The financial capital available to the Group is the essential input for making all the investments necessary to the correct function of the natural gas infrastructures.

Snam’s financial capacity comprises its own resources and debt capital obtained either on the financial markets or through its own operating income.

Infrastructural capital

The transmission network and storage and regasification plants for natural gas represent the essential infrastructural capital that allow Snam to provide operators and users with its services.

Gas pipelines, storage plants and regasification plants are the regulatory asset based (RAB) needed to obtain recognition of the reference revenues for the regulated business, as calculated on the basis of the rules defined by the Autorità di regolazione per energia reti e ambiente (ARERA).

In addition to this, in the coming years Snam’s infrastructure will be enriched with plants for the production and introduction of biomethane and natural gas distribution plants for motor vehicles

Intellectual capital

The intellectual capital is Snam’s distinctive heritage that comprises the computer systems and internal processes and procedures for the efficient management of its business activities. These practices have been developed and consolidated over time, based on company know-how and aimed at guaranteeing the safety of the networks and infrastructures for employees, suppliers and users.

Human capital

Snam’s human capital are the people making up the Group – the employees and the capillary network of Italian and international suppliers – with their wealth of knowledge and experience.

Snam supports the promotion of a business culture hinged on certain distinctive values: the optimisation and development of people, the culture of safety, the maintenance and growth of the know-how necessary for the continuous technological update and modernisation of the Group’s assets.

Relational capital

The Group’s relational capital is the “licence-to-operate” that stakeholders recognise to Snam.

The trust afforded by stakeholders in the Group’s capacity to create value is the direct consequence of more than 75 years of history that link Snam’s activities with its stakeholders and the companies in the territories hosting the infrastructures.

Also in consideration of the expansion of Snam’s business into the non-regulated market, over the next few years, the contribution made towards the enhancement of the Group’s relational capital will become increasingly important, through participation in national and international working parties and ratified agreements and understandings aiming to develop collaborations and partnerships with companies operating on the international and non-European energy markets.

Natural capital

The territory in which the infrastructures stand, the air and biodiversity are Snam’s natural capital, just like the energy resources (the natural gas) necessary to allow Snam to provide operators and users with its services.

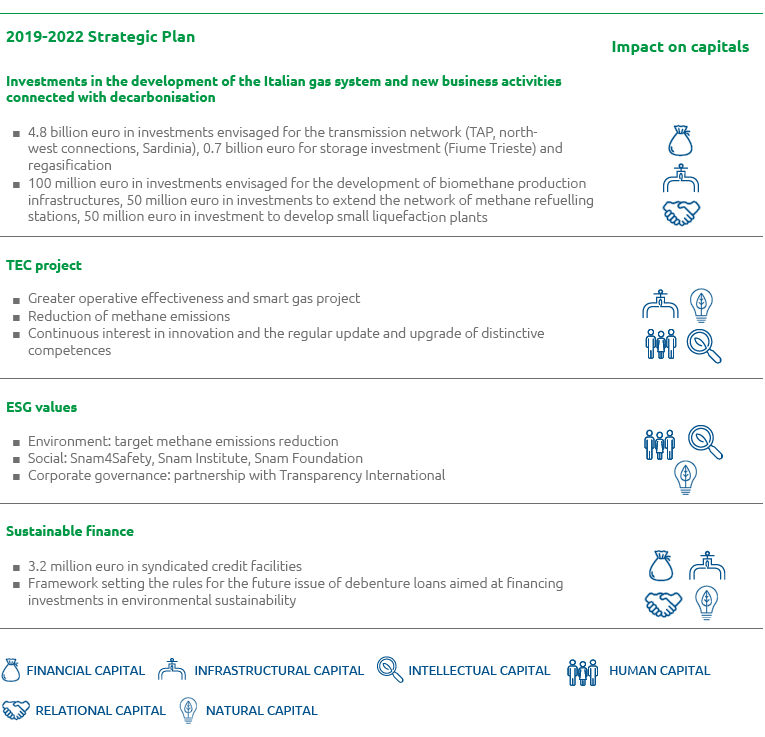

Business model

The objectives of Snam’s 2019-2022 Strategic Plan include the creation of value in all intangible capital characterising the company.

The investment programme outlined in the Strategic Plan, which envisages a total of 5.7 billion euro for the development and modernisation of the existing network and the development of new businesses connected with biomethane production and, in general, the energy transition, will have a positive impact on Snam’s financial capital.

The objectives included in the Strategic Plan shall also affect the infrastructural capital: with the aim of guaranteeing the quality and continuity of service, over the next few years, development will continue of the infrastructural and network of gas pipelines, new connections to the north-west will be completed, methanisation projects, the TAP interconnection and potential storage plants.

The energy resource is the pillar on which the Snam Group’s activity is based, acknowledging the importance of safeguarding the natural environment. As confirmation of the attention paid by the company to protecting climate, the Strategic Plan envisages a new target reduction of methane emissions.

The activities included in the TEC project will also allow Snam to enrich its natural capital, implementing actions to monitor the network and measure the territorial structure in real time, along with gas consumption and the energy efficiency of the infrastructures, thereby achieving the twofold objective of optimising operating costs and minimising the impact of its activities.

Impacts of Snam's activities on the gas system and on the energy scenario

IMPACTS ON THE GAS SYSTEM

Market facilitation With the new “Network Balancing Code” regime, which has been in effect since October 2016, the balancing service is conducted in accordance with common and harmonised European rules, which are aimed at promoting trading and market liquidity. In a new system, Users are the primary parties responsible for system equilibrium and they can balance their own trading positions (injections and withdrawals from the system) through an hourly reprogramming of their own requirements, and/or by executing gas transactions on both the organised and over-the-counter markets. Snam also performs the role of Default Transportation Supplier, namely supplies gas to Sales Companies and Final Customers for which the Balancing User responsible for the related withdrawals is not identifiable. The same service is also carried out for the Sales Companies and Final Customers at third-party transporters who explicitly requested it.

Impact of the Default Shipping Service The service in the 2017-2018 thermal year involved 192 parties amongst Final Customers and Sales Companies, for a total volume of approximately 263,300 MWh. New transmission capacity products In 2017, Snam introduced greater flexibility in offering transmission capacity at the re-delivery points that power the thermoelectric plants and the withdrawal areas through the provision of short-term capacity products (daily and monthly). In 2018, new flexibility services were also introduced, like infra-day storage auctions.

Gas access and cost The cost of transmission, distribution and metering (meter reading) services, which allow the delivery of gas to end users, is one of the three main items of the gas bill.

Incidence of the transmission service on the cost of gas The cost of the transmission service in 2018 is estimated as accounting for approximately 5% of the total costs of a typical domestic client (family with individual heating and annual consumption of 1,400 scm) as compared with 18% of the total cost of infrastructural services. New connections In 2018, 88 connection contracts were signed for the construction of new delivery/re-delivery points (of which 14 were for biomethane inputs and 43 for CNG) or the upgrading of existing points, up approximately 13% over 2017.

Creation of a european gas market Snam is one of the founders of PRISMA, the international project established to promote the harmonisation of rules for accessing and providing services in implementation of the European Codes, by offering services through a single shared digital platform. Approximately 40 European operators active in the transmission and storage of gas from 17 countries participate in the development of PRISMA.

The numbers of the PRISMA platform In 2018, the PRISMA platform further increased the number of auctions for the sale of capacity products, which in fact went from 4.5 million in 2017 to 6.5 million in 2018. The number of shippers and users registered respectively come to approximately 650 and 2,500.

Impacts of Snam's activities on the gas system and on the energy scenario

IMPACTS ON THE ENERGY SCENARIO

Security of supplies The constant, structural reduction in national production leaves Italy very much dependent on foreign gas, the import of which has recorded a 2.4% increase in the 3rd quarter of 2018 as compared with the same period of the previous year, accentuating the role played by Russia as the top supplier of Italian gas, with a share that has virtually reached 50% of the total. (Source: ENEA)

Diversification of sources Thanks to the interconnection of Snam’s network, Italy is the current European country that can rely on the greatest number of supply sources. Besides domestic production, the Italian system can receive gas through four methane import pipelines (Algeria, Libya, Russia and Norway) and 3 regasification terminals. It is also planned in the future to add the importation of gas from the Caspian Sea by constructing the TAP methane pipeline. The development of bidirectional capacity in the north of our country along the North-South corridor (reverse flow) may also make Italian supply sources accessible to other European countries. In the instance of Italy, if any of the supply sources should fail, the remaining sources of supply are capable of satisfying more than 120% of the area’s total gas demand, calculated during a day of particularly high gas demand.

Use of storage capacity In 2018, Snam took action to promote the replenishment of national storage facilities for the purpose of being able to manage seasonal peaks in demand. The replenishment level at the end of the injection campaign was 98% as opposed to a European average of 88%.

Contribution to decarbonisation Gas in its various forms guarantees lower carbon dioxide emissions, by 25% to 40% compared to other fossil fuels, as well as reduced nitrogen oxides and fine particle levels.

Gas in the national energy mix The quarterly analysis of the Italian energy system performed by ENEA highlights how, considering all the first nine months of 2018, natural gas consumption has reduced by around one percentage point on the same period of the previous year. In particular, a major reduction has been seen in consumption in the 2nd quarter (-7% in trend terms, due to the lesser thermal production linked to the resumed hydroelectric generation) and a slight increase in consumption in the 3rd quarter 2018 (+1.2% on the same quarter of 2017). Renewable energy sources (excluding biomass for thermal uses) are slightly up on the levels recorded in the 3rd quarter 2017, by approximately half a percentage point.